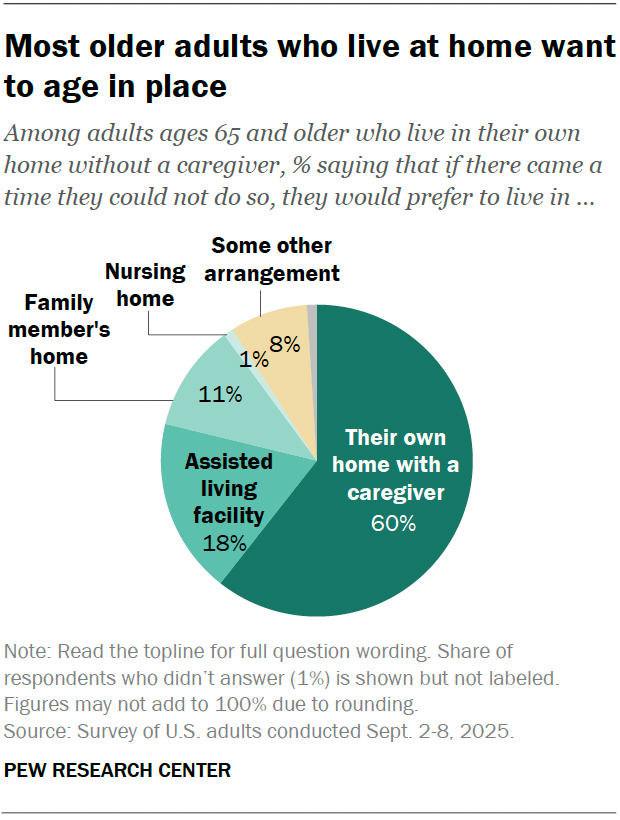

TL;DR

Senior housing occupancy reached 87.4% in Q1 2025 according to NIC MAP data, marking 13 consecutive quarters of occupancy growth. All 31 NIC MAP primary markets now exceed 80% occupancy. The top-performing markets are Boston at 92.6%, San Francisco at 90.9%, and Baltimore at 90.6%. New senior housing construction starts have dropped to just 1,076 units — the lowest level since Q2 2009. The demographic wave is building, the supply pipeline is empty, and occupancy is headed toward 90%+ nationally.

The Occupancy Story

Thirteen consecutive quarters of occupancy growth isn't a trend — it's a trajectory. Senior housing has been climbing steadily since the post-pandemic trough, and the Q1 2025 reading of 87.4% represents the highest occupancy level since 2020.

What makes this especially meaningful is the consistency. This isn't a market bouncing around. It's a sector that has posted positive absorption quarter after quarter, driven by demographics that are as predictable as anything in real estate. Baby boomers are aging. The 80+ population is expanding. And the need for professional senior care is growing every single day.

I've spent years studying the fundamentals of senior housing — including the scattered-site model that's challenging conventional wisdom — and I can tell you that what we're seeing right now is the early innings of a multi-decade demand story. The oldest boomers turned 79 in 2025, and the population of Americans aged 80+ will grow by more than 50% over the next decade. That's not a projection based on economic assumptions — it's simple demography.

U.S. Senior Housing Occupancy (2019–2026)

Senior housing occupancy has rebounded sharply from its pandemic trough, climbing steadily for over three years as the aging population drives relentless demand growth.

Think you know the facts behind the headlines?

5 questions · ~3 min

Market Leaders and Laggards

The NIC MAP data reveals significant variation across markets, and understanding that variation is essential for investors.

The leaders are impressive: - Boston: 92.6% — Driven by strong healthcare infrastructure and high barriers to new supply - San Francisco: 90.9% — Despite broader real estate challenges, senior housing demand remains robust - Baltimore: 90.6% — Benefits from proximity to major medical centers and an aging regional population

What's remarkable is that all 31 NIC MAP primary markets now exceed 80% occupancy. There are no weak markets in senior housing right now. The floor has risen dramatically, and the ceiling is still moving higher.

The markets that lagged earlier in the recovery — many in the Sun Belt where overbuilding was a concern in 2018-2019 — have now absorbed that excess supply and are approaching the national average. The recovery has been broad-based and durable.

The Construction Drought

Here's the number that should stop every investor in their tracks: only 1,076 new senior housing units were started in Q1 2025. That's the lowest level since Q2 2009, when the industry was reeling from the financial crisis.

To put this in context, the senior housing industry was starting 10,000+ units per quarter as recently as 2019. The construction pipeline has collapsed by roughly 90%. The reasons are familiar — higher construction costs (amplified by tariffs), elevated interest rates, and tighter construction lending — but the implications for existing operators are profound.

Less new supply means existing communities fill up faster. It means operators have pricing power. And it means the gap between demand and supply is widening, not narrowing. For investors who own or acquire senior housing assets today, the supply drought is creating a tailwind that will persist for years.

Senior Housing Quarterly Construction Starts (Units, 2019–2025)

New senior housing starts have cratered to levels not seen in over 15 years, creating a supply gap that will take years to fill even as demand accelerates.

Why This Matters for Investors

At F6 Partners, senior housing is one of our core conviction sectors, and the Q1 2025 data reinforces everything we've been telling our investors.

The investment case is built on three pillars:

- Demographics are destiny. The 80+ population growth is locked in and accelerating. No recession, policy change, or market disruption alters the fundamental demand trajectory.

- Supply is structurally constrained. With construction starts at 16-year lows, the supply response to rising demand will take years to materialize. Existing assets benefit enormously from this imbalance.

- Operating fundamentals are improving. Higher occupancy translates to better operating margins, stronger cash flows, and enhanced property values. The path from 87.4% toward 90%+ represents significant value creation for well-operated communities.

I'll add a personal note here. My family is everything to me, and watching the senior housing industry evolve toward more compassionate, hospitality-driven care gives me genuine hope. The best senior housing operators today aren't just running buildings — they're creating communities where our parents and grandparents can age with dignity. That's a mission worth investing in, and the returns follow when the mission is right.

The 87.4% occupancy figure is a milestone, but it's not the destination. With demographics accelerating and supply constrained, I believe we'll see national occupancy cross 90% within the next 12-18 months. For investors positioned in this sector, the best is yet to come.

U.S. Population Aged 80+ (Millions, 2019–2026)

The 80-plus population is entering a steep growth trajectory that will add millions of potential senior housing residents over the next decade.

TL;DR

Senior housing occupancy reached 87.4% in Q1 2025 according to NIC MAP data, marking 13 consecutive quarters of occupancy growth. All 31 NIC MAP primary markets now exceed 80% occupancy. The top-performing markets are Boston at 92.6%, San Francisco at 90.9%, and Baltimore at 90.6%. New senior housing construction starts have dropped to just 1,076 units — the lowest level since Q2 2009. The demographic wave is building, the supply pipeline is empty, and occupancy is headed toward 90%+ nationally.

The Occupancy Story

Thirteen consecutive quarters of occupancy growth isn't a trend — it's a trajectory. Senior housing has been climbing steadily since the post-pandemic trough, and the Q1 2025 reading of 87.4% represents the highest occupancy level since 2020.

What makes this especially meaningful is the consistency. This isn't a market bouncing around. It's a sector that has posted positive absorption quarter after quarter, driven by demographics that are as predictable as anything in real estate. Baby boomers are aging. The 80+ population is expanding. And the need for professional senior care is growing every single day.

I've spent years studying the fundamentals of senior housing — including the scattered-site model that's challenging conventional wisdom — and I can tell you that what we're seeing right now is the early innings of a multi-decade demand story. The oldest boomers turned 79 in 2025, and the population of Americans aged 80+ will grow by more than 50% over the next decade. That's not a projection based on economic assumptions — it's simple demography.

U.S. Senior Housing Occupancy (2019–2026)

Senior housing occupancy has rebounded sharply from its pandemic trough, climbing steadily for over three years as the aging population drives relentless demand growth.

Think you know the facts behind the headlines?

5 questions · ~3 min

Market Leaders and Laggards

The NIC MAP data reveals significant variation across markets, and understanding that variation is essential for investors.

The leaders are impressive: - Boston: 92.6% — Driven by strong healthcare infrastructure and high barriers to new supply - San Francisco: 90.9% — Despite broader real estate challenges, senior housing demand remains robust - Baltimore: 90.6% — Benefits from proximity to major medical centers and an aging regional population

What's remarkable is that all 31 NIC MAP primary markets now exceed 80% occupancy. There are no weak markets in senior housing right now. The floor has risen dramatically, and the ceiling is still moving higher.

The markets that lagged earlier in the recovery — many in the Sun Belt where overbuilding was a concern in 2018-2019 — have now absorbed that excess supply and are approaching the national average. The recovery has been broad-based and durable.

The Construction Drought

Here's the number that should stop every investor in their tracks: only 1,076 new senior housing units were started in Q1 2025. That's the lowest level since Q2 2009, when the industry was reeling from the financial crisis.

To put this in context, the senior housing industry was starting 10,000+ units per quarter as recently as 2019. The construction pipeline has collapsed by roughly 90%. The reasons are familiar — higher construction costs (amplified by tariffs), elevated interest rates, and tighter construction lending — but the implications for existing operators are profound.

Less new supply means existing communities fill up faster. It means operators have pricing power. And it means the gap between demand and supply is widening, not narrowing. For investors who own or acquire senior housing assets today, the supply drought is creating a tailwind that will persist for years.

Senior Housing Quarterly Construction Starts (Units, 2019–2025)

New senior housing starts have cratered to levels not seen in over 15 years, creating a supply gap that will take years to fill even as demand accelerates.

Why This Matters for Investors

At F6 Partners, senior housing is one of our core conviction sectors, and the Q1 2025 data reinforces everything we've been telling our investors.

The investment case is built on three pillars:

- Demographics are destiny. The 80+ population growth is locked in and accelerating. No recession, policy change, or market disruption alters the fundamental demand trajectory.

- Supply is structurally constrained. With construction starts at 16-year lows, the supply response to rising demand will take years to materialize. Existing assets benefit enormously from this imbalance.

- Operating fundamentals are improving. Higher occupancy translates to better operating margins, stronger cash flows, and enhanced property values. The path from 87.4% toward 90%+ represents significant value creation for well-operated communities.

I'll add a personal note here. My family is everything to me, and watching the senior housing industry evolve toward more compassionate, hospitality-driven care gives me genuine hope. The best senior housing operators today aren't just running buildings — they're creating communities where our parents and grandparents can age with dignity. That's a mission worth investing in, and the returns follow when the mission is right.

The 87.4% occupancy figure is a milestone, but it's not the destination. With demographics accelerating and supply constrained, I believe we'll see national occupancy cross 90% within the next 12-18 months. For investors positioned in this sector, the best is yet to come.

U.S. Population Aged 80+ (Millions, 2019–2026)

The 80-plus population is entering a steep growth trajectory that will add millions of potential senior housing residents over the next decade.

Test Your Knowledge

How well do you know senior housing markets?

Andrew LeBaron