A Little Over Five Years Ago, I Bought a Motel 6 (it was actually a Studio 6, which is the extended stay version of a Motel 6).

I converted it into an apartment-style extended stay called Pinetop Studio Suites.

I tell that story a lot, and not because it is the most sophisticated deal in my portfolio. I tell it because it is the cleanest one. I bought it. I executed on it. I refinanced it. I held it through a cycle that nobody who underwrote that asset in 2020 had on the bingo card. The numbers are documented, the property is operating, and the result is on paper. One deal. One cycle. One honest story.

That deal is the floor of every conversation I have with a family office in 2026. Not the ceiling. The floor.

One Deal. One Cycle. One Honest Story. That Is the Floor.

Five years ago, an operator could walk into a family office meeting with a slide that said "we have done $400 million across 18 deals since 2014" and the conversation moved straight to the data room. In 2026 that slide gets you a polite follow-up email and nothing else.

What changed is not the politeness of family offices. What changed is the cost of capital, the math underneath every deal, and the dawning realization that almost every track record you saw before 2022 was assembled inside a regime that has not existed for three years. The bar is no longer "have you done a lot of deals." The bar is "have you done one deal that proves you can operate in this rate environment, on these debt terms, with these cap rates, and tell me the truth about it."

TL;DR

Family offices wrote $7.5B of direct real estate checks in H1 2025, up from $2.1B in H1 2023 (FINTRX). Real estate is now their #1 asset class at 39% of allocations, up from 26% two years earlier. 44% prefer direct over fund commitments and 69% of deal flow is club deals. 5%+ GP co-investment is the new floor. The single sharpest filter being applied across IC desks is whether the operator has closed one full-cycle deal that started after Q1 2022. Pre-2022 track records, no matter how impressive, are being filed under "different cycle." Roughly $875B of CRE debt matures in 2026 (Mortgage Bankers Association), with the wall peaking at $1.26T in 2027 (Trepp). The next 12 months are going to sort the operators who cleared the filter from the operators who did not.

I. The 2026 Family Office Decision

Family offices are not retreating from real estate. They are concentrating into it. J.P. Morgan's Global Family Office Report and FINTRX's 2025 Family Office Real Estate Report both confirm the same trend from different angles: real estate has moved from a meaningful slice of the family office portfolio to the largest single allocation across the cohort.

The shape of how that capital is being deployed has also changed. 44% of family offices now prefer direct investment over fund commitments, and 69% of family office deal flow now runs through club deals where multiple families co-invest alongside an operator. Minimum check sizes have dropped from the historical $5-10M floor down to $250K-$500K in many vehicles. The pool of family offices that can write a real estate check has widened considerably. The pool of operators they will write that check to has narrowed sharply.

That is the entire game in 2026: more capital, fewer operators it is willing to back.

II. Why Pre-2022 Track Records Stopped Working

In March 2022 the Federal Reserve began the most aggressive hiking cycle in 40 years. The cost of capital tripled inside 18 months. Cap rates expanded 100 to 200 bps depending on sector. Refi math broke for any deal underwritten to 2019 or 2021 assumptions. The operating playbook that worked at zero percent rates does not work at four percent rates. None of this is news to anyone reading this.

What is news, or at least what has crystallized in the last six months across family office IC conversations, is the conclusion: the cycle that ended in 2022 is now treated as a different asset class, not a different vintage. A great 2018 to 2021 track record is being read the way an institutional LP reads a great 2005 to 2007 track record: as evidence that the operator could ride a tailwind. Not as evidence that the operator can navigate a headwind.

This is not unfair. It is structural. The IRR you generated on a deal you bought in 2019 with 70% LTV agency debt at 3.4% is not a number you can replicate in 2026 with 60% LTV bridge debt at 7.8%. Family offices have figured this out and are pricing accordingly. They are not asking you to apologize for a great pre-2022 track record. They are asking you to prove you can do it again, now, on these terms.

A great 2018 to 2021 track record proves you could ride a tailwind. It does not prove you can navigate a headwind. Family offices have stopped accepting the first as evidence of the second.

— Andrew LeBaron

III. The Five Track Record Lies

There are five common ways operators are presenting pre-2022 track records that family office IC desks have learned to spot in the first 90 seconds.

The "blended IRR" that hides the post-2022 deals. A 22% blended IRR across 14 deals where 12 of those deals were sold or refinanced before March 2022. The post-2022 deals, the ones that actually test the operator, are a footnote.

The "extended" deal. A deal that hit its original pro forma exit date in 2024, did not refinance cleanly, got an extension from the lender at 200 bps over original terms, and is presented as "performing." This is the single most common presentation issue in 2026.

The "soft IRR" on a deal still in the hold. An IRR projection on a current deal where the only realized component is the acquisition itself. The number is real on paper and unrealized in fact.

The "team that did it elsewhere" track record. The principal personally executed great deals at a prior firm but the current entity has not closed a full cycle. The track record is borrowed.

The "all-asset-class" portfolio with no mention of the asset class being raised for. A great industrial track record being used to raise for a hotel-to-residential conversion fund. Family offices used to allow this. They no longer do.

IV. The Seven-Question Operator Filter

Here are the seven questions I have heard across multiple family office IC desks in the last six months. They are not hypothetical. They are the actual filter being applied. If you cannot answer all seven cleanly, in writing, with documents, you are not getting past the gatekeeper.

Tap any card to expand the full prompt, what the IC desk is actually testing, the answer that clears the filter, and the answer that ends the meeting. Frameworks like the ones REALM and MMG Real Estate Advisors publish are useful for grounding question seven if you want a starting point.

If you cannot answer all seven of these questions cleanly, in writing, with documents to back them up, you are not getting past the family office gatekeeper in 2026.

— Andrew LeBaron

V. The Math That Forces the Filter

The reason the filter exists is not that family offices became more demanding. The reason the filter exists is that the math underneath every CRE deal got harder.

Roughly $875B of commercial mortgage debt matures in 2026 per the MBA's February 2026 survey. Trepp's broader cumulative 2025 to 2026 figure is roughly $1.8T. The wall peaks at $1.26T in 2027, the largest single-year maturity in U.S. CRE history. Multifamily alone jumps 56% year over year, from $104B in 2025 to $162B in 2026.

Per MSCI Real Capital Analytics, values on transacted assets are still well below 2022 peaks across most sectors. The bid-ask gap that paralyzed 2024 is starting to close, but it is closing through price discovery on the seller's side, not through capital flooding back in on the buyer's side. Family offices know this. They know that the next 24 months will produce more genuine distress than the prior 24 months produced rumored distress. They are not interested in operators who survived the easy cycle. They are interested in operators who can underwrite, acquire, and execute on the hard one.

VI. What "Family Office Approved" Actually Means in 2026

Family office approved is not a logo, a designation, or an introduction. In 2026 it means an operator who has cleared the seven-question filter, whose data room contains documented post-2022 execution, whose GP co-investment is meaningful, and whose property-level reporting is institutional grade.

The cohort of operators who meet this bar is meaningfully smaller than the cohort that was raising in 2021. The cohort of family offices actively writing checks is meaningfully larger. The result is that operators who clear the filter are seeing more inbound interest than they have seen in five years, and operators who do not are seeing the lights go off entirely.

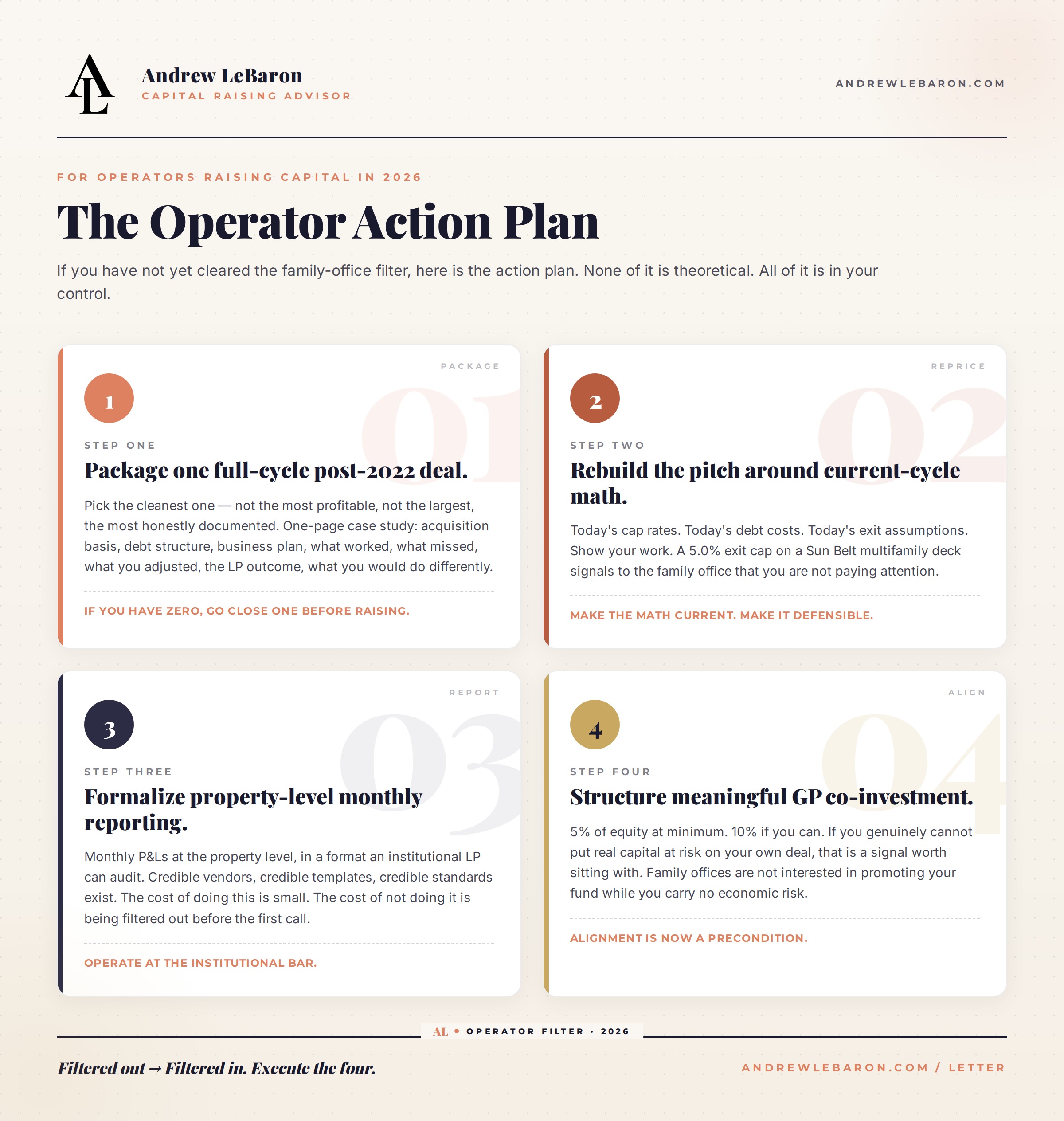

VII. The Operator Action Plan: Four Steps

If you are an operator who has not yet cleared the filter, here is the action plan. None of it is theoretical. All of it is in your control.

Step 1: Package one full-cycle post-2022 deal.

Pick the cleanest one. It does not have to be the most profitable. It does not have to be the largest. It has to be the most honestly documented. Write a one-page case study with the acquisition basis, the debt structure, the business plan, what worked, what missed, what you adjusted, what the LP outcome was, and what you would do differently. If you have more than one, package the best one first and the others as appendix material. If you have zero, you have a different problem and the answer is to go close one before raising for anything else.

Step 2: Rebuild the pitch around current-cycle math.

Today's cap rates. Today's debt costs. Today's exit assumptions. Show your work. If your pitch deck still has a 5.0% exit cap on a multifamily deal in a Sun Belt market, you are signaling to the family office that you are not paying attention. Use the MMG Real Estate Advisors framework or your own, but make it current.

Step 3: Formalize property-level monthly reporting.

If you are not already producing monthly P&Ls at the property level, in a format that an institutional LP can audit, you are operating below the bar. There are credible vendors, credible templates, and credible standards. Adopt them. The cost of doing this is small. The cost of not doing it is being filtered out before the first call.

Step 4: Structure meaningful GP co-investment.

5% of equity at minimum. 10% if you can. If you genuinely cannot put real capital at risk on your own deal, that is a signal worth sitting with. Family offices are not interested in promoting your fund for you while you carry no economic risk.

The operators who clear the filter in the next 90 days will compete in a market where most of their peers cannot credibly raise. That is the entire ballgame.

— Andrew LeBaron

VIII. The Capital That Is Actually Moving Right Now

The capital is moving. PERE reported $164.4B of global real estate fundraising through the first three quarters of 2025, with $115B targeting North America. Blackstone has publicly cited $65B+ of real estate dry powder. Apollo, Brookfield, and Ares are all raising into supply. Family offices are increasing their direct allocations. The capital is there. The filter for who gets it has tightened.

IX. The Bottom Line

The motel I bought five years ago is still operating. The conversion held up. The investors got paid. None of that is special on its own. What is special, and what every operator competing for family office capital in 2026 has to internalize, is that one honestly executed full-cycle deal in this rate environment is now the floor of credibility, not the ceiling.

If you have one, package it cleanly and get it in front of the right capital. Want a working session on how to structure that conversation? Book a 30-minute call at /meetwithandrew. I do them every week with operators who are at this exact inflection point.

If you do not have one yet, focus there first. Close one deal in the current cycle and do it cleanly. The capital will follow the proof, in that order. The operators who cleared the filter in the last six months are already in serious conversations. The operators who clear it in the next 90 days will compete in a market where most of their peers cannot credibly raise. That is the entire ballgame.

Want my checklist for the seven-question filter and the four-step action plan in a single one-pager you can stress test against your own pipeline? Grab a 1:1 working session at /meetwithandrew and I will walk you through it.

— Andrew

Sources & References

- FINTRX Family Office Real Estate Report 2025

- J.P. Morgan Global Family Office Report 2026

- Mortgage Bankers Association CRE Maturity Survey, February 2026

- Trepp CMBS Maturity Wall Data

- MSCI Real Capital Analytics

- MMG Real Estate Advisors Multifamily Outlook

- REALM (Real Estate Asset Leaders Network)

- PERE Q4 2025 Fundraising Report

- Campden Wealth Global Family Office Report

- Federal Reserve FOMC Calendar

Frequently Asked Questions

Q: What is the family office operator filter?

It is the set of criteria family offices are using in 2026 to decide which real estate operators get a serious capital conversation. The single sharpest test is whether the operator has closed at least one full-cycle deal that started after Q1 2022, in the current rate environment, with documented property-level results. Pre-2022 track records, no matter how impressive, are increasingly being treated as evidence of a different cycle, not the current one.

Q: Why did pre-2022 track records stop working?

The Fed began hiking in March 2022 and the cost of capital tripled within 18 months. Cap rates expanded 100 to 200 bps depending on sector, refi math broke for any deal underwritten to 2019 or 2021 assumptions, and the operational playbook that worked in a 0% rate environment does not work in a 4%+ rate environment. Family offices have concluded that a great 2018 to 2021 track record proves you could ride a tailwind, not that you can navigate a headwind.

Q: What are the seven questions family offices are asking?

1) Have you closed at least one full-cycle deal that started after Q1 2022?

2) Did your last deal hit pro forma, miss it, or get refinanced into "extend and pretend"?

3) What is your current portfolio's debt service coverage ratio at today's rates?

4) How much GP capital is in your last three deals?

5) Who is your lender on your last new origination, and what were the terms?

6) Show me the property-level monthly operating reports for your last 12 months.

7) What is your specific thesis on the 2026 to 2028 vintage, and how is your fund structured to capture it?

Q: How much GP co-investment do family offices expect now?

5% or more of the equity stack is the new floor at most family office IC desks, up from the 1-2% historical norm. Some family offices will not consider an operator without 10%+ GP co-investment. The reasoning is simple: alignment used to be a soft preference; in this cycle, it is a hard precondition.

Q: What is the four-step action plan for operators?

Step 1: package one full-cycle post-2022 deal with clean monthly operating data. Step 2: rebuild the pitch around current-cycle math (today's cap rates, today's debt costs, today's exit assumptions). Step 3: formalize property-level monthly reporting using institutional-grade tooling. Step 4: structure meaningful GP co-investment of at least 5% of equity. Operators who execute these four steps move from filtered out to filtered in.

Q: How is family office capital actually being deployed in 2026?

44% of family offices now prefer direct investment over fund commitments, and 69% of deal flow runs through club deals where multiple family offices co-invest alongside an operator. The minimum check size has dropped from the historical $5-10M down to $250K-$500K in many vehicles, broadening the pool of operators who can credibly raise family office capital, but only those who clear the operator filter.

Q: Is this only a multifamily story?

No. The same filter is being applied across every CRE sector: multifamily, industrial, office-to-residential conversions, hotel, self-storage, IOS, manufactured housing, student housing, and senior housing. The asset class matters less than the operator's ability to demonstrate one full-cycle execution in the current rate environment.

A Little Over Five Years Ago, I Bought a Motel 6 (it was actually a Studio 6, which is the extended stay version of a Motel 6).

I converted it into an apartment-style extended stay called Pinetop Studio Suites.

I tell that story a lot, and not because it is the most sophisticated deal in my portfolio. I tell it because it is the cleanest one. I bought it. I executed on it. I refinanced it. I held it through a cycle that nobody who underwrote that asset in 2020 had on the bingo card. The numbers are documented, the property is operating, and the result is on paper. One deal. One cycle. One honest story.

That deal is the floor of every conversation I have with a family office in 2026. Not the ceiling. The floor.

One Deal. One Cycle. One Honest Story. That Is the Floor.

Five years ago, an operator could walk into a family office meeting with a slide that said "we have done $400 million across 18 deals since 2014" and the conversation moved straight to the data room. In 2026 that slide gets you a polite follow-up email and nothing else.

What changed is not the politeness of family offices. What changed is the cost of capital, the math underneath every deal, and the dawning realization that almost every track record you saw before 2022 was assembled inside a regime that has not existed for three years. The bar is no longer "have you done a lot of deals." The bar is "have you done one deal that proves you can operate in this rate environment, on these debt terms, with these cap rates, and tell me the truth about it."

TL;DR

Family offices wrote $7.5B of direct real estate checks in H1 2025, up from $2.1B in H1 2023 (FINTRX). Real estate is now their #1 asset class at 39% of allocations, up from 26% two years earlier. 44% prefer direct over fund commitments and 69% of deal flow is club deals. 5%+ GP co-investment is the new floor. The single sharpest filter being applied across IC desks is whether the operator has closed one full-cycle deal that started after Q1 2022. Pre-2022 track records, no matter how impressive, are being filed under "different cycle." Roughly $875B of CRE debt matures in 2026 (Mortgage Bankers Association), with the wall peaking at $1.26T in 2027 (Trepp). The next 12 months are going to sort the operators who cleared the filter from the operators who did not.

I. The 2026 Family Office Decision

Family offices are not retreating from real estate. They are concentrating into it. J.P. Morgan's Global Family Office Report and FINTRX's 2025 Family Office Real Estate Report both confirm the same trend from different angles: real estate has moved from a meaningful slice of the family office portfolio to the largest single allocation across the cohort.

The shape of how that capital is being deployed has also changed. 44% of family offices now prefer direct investment over fund commitments, and 69% of family office deal flow now runs through club deals where multiple families co-invest alongside an operator. Minimum check sizes have dropped from the historical $5-10M floor down to $250K-$500K in many vehicles. The pool of family offices that can write a real estate check has widened considerably. The pool of operators they will write that check to has narrowed sharply.

That is the entire game in 2026: more capital, fewer operators it is willing to back.

II. Why Pre-2022 Track Records Stopped Working

In March 2022 the Federal Reserve began the most aggressive hiking cycle in 40 years. The cost of capital tripled inside 18 months. Cap rates expanded 100 to 200 bps depending on sector. Refi math broke for any deal underwritten to 2019 or 2021 assumptions. The operating playbook that worked at zero percent rates does not work at four percent rates. None of this is news to anyone reading this.

What is news, or at least what has crystallized in the last six months across family office IC conversations, is the conclusion: the cycle that ended in 2022 is now treated as a different asset class, not a different vintage. A great 2018 to 2021 track record is being read the way an institutional LP reads a great 2005 to 2007 track record: as evidence that the operator could ride a tailwind. Not as evidence that the operator can navigate a headwind.

This is not unfair. It is structural. The IRR you generated on a deal you bought in 2019 with 70% LTV agency debt at 3.4% is not a number you can replicate in 2026 with 60% LTV bridge debt at 7.8%. Family offices have figured this out and are pricing accordingly. They are not asking you to apologize for a great pre-2022 track record. They are asking you to prove you can do it again, now, on these terms.

A great 2018 to 2021 track record proves you could ride a tailwind. It does not prove you can navigate a headwind. Family offices have stopped accepting the first as evidence of the second.

— Andrew LeBaron

III. The Five Track Record Lies

There are five common ways operators are presenting pre-2022 track records that family office IC desks have learned to spot in the first 90 seconds.

The "blended IRR" that hides the post-2022 deals. A 22% blended IRR across 14 deals where 12 of those deals were sold or refinanced before March 2022. The post-2022 deals, the ones that actually test the operator, are a footnote.

The "extended" deal. A deal that hit its original pro forma exit date in 2024, did not refinance cleanly, got an extension from the lender at 200 bps over original terms, and is presented as "performing." This is the single most common presentation issue in 2026.

The "soft IRR" on a deal still in the hold. An IRR projection on a current deal where the only realized component is the acquisition itself. The number is real on paper and unrealized in fact.

The "team that did it elsewhere" track record. The principal personally executed great deals at a prior firm but the current entity has not closed a full cycle. The track record is borrowed.

The "all-asset-class" portfolio with no mention of the asset class being raised for. A great industrial track record being used to raise for a hotel-to-residential conversion fund. Family offices used to allow this. They no longer do.

IV. The Seven-Question Operator Filter

Here are the seven questions I have heard across multiple family office IC desks in the last six months. They are not hypothetical. They are the actual filter being applied. If you cannot answer all seven cleanly, in writing, with documents, you are not getting past the gatekeeper.

Tap any card to expand the full prompt, what the IC desk is actually testing, the answer that clears the filter, and the answer that ends the meeting. Frameworks like the ones REALM and MMG Real Estate Advisors publish are useful for grounding question seven if you want a starting point.

If you cannot answer all seven of these questions cleanly, in writing, with documents to back them up, you are not getting past the family office gatekeeper in 2026.

— Andrew LeBaron

V. The Math That Forces the Filter

The reason the filter exists is not that family offices became more demanding. The reason the filter exists is that the math underneath every CRE deal got harder.

Roughly $875B of commercial mortgage debt matures in 2026 per the MBA's February 2026 survey. Trepp's broader cumulative 2025 to 2026 figure is roughly $1.8T. The wall peaks at $1.26T in 2027, the largest single-year maturity in U.S. CRE history. Multifamily alone jumps 56% year over year, from $104B in 2025 to $162B in 2026.

Per MSCI Real Capital Analytics, values on transacted assets are still well below 2022 peaks across most sectors. The bid-ask gap that paralyzed 2024 is starting to close, but it is closing through price discovery on the seller's side, not through capital flooding back in on the buyer's side. Family offices know this. They know that the next 24 months will produce more genuine distress than the prior 24 months produced rumored distress. They are not interested in operators who survived the easy cycle. They are interested in operators who can underwrite, acquire, and execute on the hard one.

VI. What "Family Office Approved" Actually Means in 2026

Family office approved is not a logo, a designation, or an introduction. In 2026 it means an operator who has cleared the seven-question filter, whose data room contains documented post-2022 execution, whose GP co-investment is meaningful, and whose property-level reporting is institutional grade.

The cohort of operators who meet this bar is meaningfully smaller than the cohort that was raising in 2021. The cohort of family offices actively writing checks is meaningfully larger. The result is that operators who clear the filter are seeing more inbound interest than they have seen in five years, and operators who do not are seeing the lights go off entirely.

VII. The Operator Action Plan: Four Steps

If you are an operator who has not yet cleared the filter, here is the action plan. None of it is theoretical. All of it is in your control.

Step 1: Package one full-cycle post-2022 deal.

Pick the cleanest one. It does not have to be the most profitable. It does not have to be the largest. It has to be the most honestly documented. Write a one-page case study with the acquisition basis, the debt structure, the business plan, what worked, what missed, what you adjusted, what the LP outcome was, and what you would do differently. If you have more than one, package the best one first and the others as appendix material. If you have zero, you have a different problem and the answer is to go close one before raising for anything else.

Step 2: Rebuild the pitch around current-cycle math.

Today's cap rates. Today's debt costs. Today's exit assumptions. Show your work. If your pitch deck still has a 5.0% exit cap on a multifamily deal in a Sun Belt market, you are signaling to the family office that you are not paying attention. Use the MMG Real Estate Advisors framework or your own, but make it current.

Step 3: Formalize property-level monthly reporting.

If you are not already producing monthly P&Ls at the property level, in a format that an institutional LP can audit, you are operating below the bar. There are credible vendors, credible templates, and credible standards. Adopt them. The cost of doing this is small. The cost of not doing it is being filtered out before the first call.

Step 4: Structure meaningful GP co-investment.

5% of equity at minimum. 10% if you can. If you genuinely cannot put real capital at risk on your own deal, that is a signal worth sitting with. Family offices are not interested in promoting your fund for you while you carry no economic risk.

The operators who clear the filter in the next 90 days will compete in a market where most of their peers cannot credibly raise. That is the entire ballgame.

— Andrew LeBaron

VIII. The Capital That Is Actually Moving Right Now

The capital is moving. PERE reported $164.4B of global real estate fundraising through the first three quarters of 2025, with $115B targeting North America. Blackstone has publicly cited $65B+ of real estate dry powder. Apollo, Brookfield, and Ares are all raising into supply. Family offices are increasing their direct allocations. The capital is there. The filter for who gets it has tightened.

IX. The Bottom Line

The motel I bought five years ago is still operating. The conversion held up. The investors got paid. None of that is special on its own. What is special, and what every operator competing for family office capital in 2026 has to internalize, is that one honestly executed full-cycle deal in this rate environment is now the floor of credibility, not the ceiling.

If you have one, package it cleanly and get it in front of the right capital. Want a working session on how to structure that conversation? Book a 30-minute call at /meetwithandrew. I do them every week with operators who are at this exact inflection point.

If you do not have one yet, focus there first. Close one deal in the current cycle and do it cleanly. The capital will follow the proof, in that order. The operators who cleared the filter in the last six months are already in serious conversations. The operators who clear it in the next 90 days will compete in a market where most of their peers cannot credibly raise. That is the entire ballgame.

Want my checklist for the seven-question filter and the four-step action plan in a single one-pager you can stress test against your own pipeline? Grab a 1:1 working session at /meetwithandrew and I will walk you through it.

— Andrew

Sources & References

- FINTRX Family Office Real Estate Report 2025

- J.P. Morgan Global Family Office Report 2026

- Mortgage Bankers Association CRE Maturity Survey, February 2026

- Trepp CMBS Maturity Wall Data

- MSCI Real Capital Analytics

- MMG Real Estate Advisors Multifamily Outlook

- REALM (Real Estate Asset Leaders Network)

- PERE Q4 2025 Fundraising Report

- Campden Wealth Global Family Office Report

- Federal Reserve FOMC Calendar

Frequently Asked Questions

Q: What is the family office operator filter?

It is the set of criteria family offices are using in 2026 to decide which real estate operators get a serious capital conversation. The single sharpest test is whether the operator has closed at least one full-cycle deal that started after Q1 2022, in the current rate environment, with documented property-level results. Pre-2022 track records, no matter how impressive, are increasingly being treated as evidence of a different cycle, not the current one.

Q: Why did pre-2022 track records stop working?

The Fed began hiking in March 2022 and the cost of capital tripled within 18 months. Cap rates expanded 100 to 200 bps depending on sector, refi math broke for any deal underwritten to 2019 or 2021 assumptions, and the operational playbook that worked in a 0% rate environment does not work in a 4%+ rate environment. Family offices have concluded that a great 2018 to 2021 track record proves you could ride a tailwind, not that you can navigate a headwind.

Q: What are the seven questions family offices are asking?

1) Have you closed at least one full-cycle deal that started after Q1 2022?

2) Did your last deal hit pro forma, miss it, or get refinanced into "extend and pretend"?

3) What is your current portfolio's debt service coverage ratio at today's rates?

4) How much GP capital is in your last three deals?

5) Who is your lender on your last new origination, and what were the terms?

6) Show me the property-level monthly operating reports for your last 12 months.

7) What is your specific thesis on the 2026 to 2028 vintage, and how is your fund structured to capture it?

Q: How much GP co-investment do family offices expect now?

5% or more of the equity stack is the new floor at most family office IC desks, up from the 1-2% historical norm. Some family offices will not consider an operator without 10%+ GP co-investment. The reasoning is simple: alignment used to be a soft preference; in this cycle, it is a hard precondition.

Q: What is the four-step action plan for operators?

Step 1: package one full-cycle post-2022 deal with clean monthly operating data. Step 2: rebuild the pitch around current-cycle math (today's cap rates, today's debt costs, today's exit assumptions). Step 3: formalize property-level monthly reporting using institutional-grade tooling. Step 4: structure meaningful GP co-investment of at least 5% of equity. Operators who execute these four steps move from filtered out to filtered in.

Q: How is family office capital actually being deployed in 2026?

44% of family offices now prefer direct investment over fund commitments, and 69% of deal flow runs through club deals where multiple family offices co-invest alongside an operator. The minimum check size has dropped from the historical $5-10M down to $250K-$500K in many vehicles, broadening the pool of operators who can credibly raise family office capital, but only those who clear the operator filter.

Q: Is this only a multifamily story?

No. The same filter is being applied across every CRE sector: multifamily, industrial, office-to-residential conversions, hotel, self-storage, IOS, manufactured housing, student housing, and senior housing. The asset class matters less than the operator's ability to demonstrate one full-cycle execution in the current rate environment.

Andrew LeBaron